Cooper-Standard

Disclaimer: The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. You are advised to discuss your investment options with your financial advisers. Consult your financial adviser to understand whether any investment is suitable for your specific needs. I may, from time to time, have positions in the securities covered in the articles on this website. This is not a recommendation to buy or sell stocks.

Background

Cooper Standard designs and manufactures sealing systems that protect vehicle interiors from weather, dust and noise intrusion; fuel and brake delivery systems that sense, deliver and control fluids to fuel and brake systems; and fluid transfer systems that sense, deliver and control fluids and vapors for optimal powertrain and HVAC operation. These systems are used in passenger vehicles and light trucks manufactured by global automotive original equipment manufacturers (“OEMs”). 82% of 2022 sales were made to major OEMs with top customers Ford (25%) and GM (19%) and Stellantis (14%).

The auto industry is characterized by high barriers to entry due to start-up costs and long-standing customer relationships. CEO Jeffrey Edwards emphasized their stellar reputation: “We have relationships with the top of our customers’ engineering houses. We’re well known. 60 years of building relationships. We’re trusted. You don’t go back in and ask the type of pricing help that we’ve done the last 1.5 years and not be good at what you do because if you aren’t, you’d be thrown out faster than you showed up. And so we’re confident that they want us. We’re confident that our innovation is a big part of that, and we’re confident that our ability to execute for them has never been better” (J.P. Morgan Auto Conference, August 2023).

Once a product of an automotive supplier is included in an OEM’s platform, the revenue becomes predictable for the life of the contract (usually 5 years), though still subject to the cyclical nature of the auto industry. Typically the contracts are renewed as long as they are successfully fulfilled. To reduce production costs, OEMs source many products from a single supplier; therefore, a global manufacturing and delivery footprint is critical to winning and fulfilling global contracts.

Investment Case:

I found CPS through Tom Hayes’ podcast Hedge Fund Tips with Tom Hayes. Tom recounts purchasing the stock in 2022 amidst bankruptcy fears, and his belief that they would be able to refinance their debt due to their high asset coverage. Tom also compares the situation to Charlie Munger’s famous bet on “Tenneco”, another auto components supplier, which resulted in an 8x return over two years (starting at 2’16”).

My investment case for CPS is based on the following:

Normalization of automotive production based on the aging U.S. car fleet and easing post-covid supply chain challenges.

Operational leverage that will increase margins at higher production levels.

Electric and hybrid vehicle opportunities.

Innovative new product lines.

Operational improvements resulting in a lean cost structure.

Aligned management team and ROIC focus.

Below I will discuss each point in detail:

Normalization of automotive production.

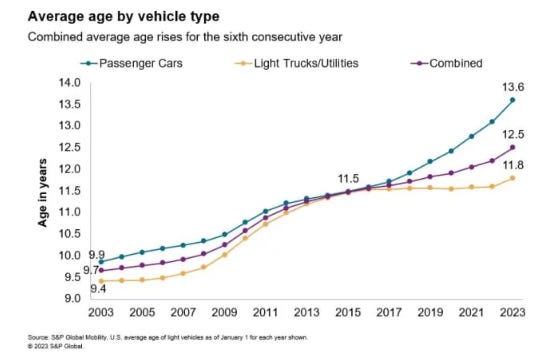

The average age of vehicles in the U.S. has reached a record 12.5 years, according to S&P Global Mobility.

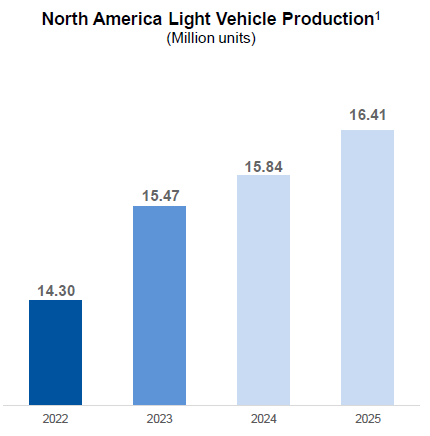

Vehicle production is gradually returning to pre-covid levels. In July 2023, S&P Global estimated the following North American light vehicle production levels for the next two years:

At the J.P. Morgan Auto Conference in August 2023, CEO Jeffrey Edwards summarized his expectations for returning industry-wide production levels:

North America: 16-17 million units.

Europe: 21-22 million units.

China: 28 million units.

South America + Asia (ex-China): ~33 million units

Globally: ~100 million units.

Post-covid supply chain and labor market disruptions as well as labor union strikes have challenged the auto industry in recent years. At the J.P. Morgan Auto Conference, Edwards said that supply chain bottlenecks including the semiconductor chip shortage have “stabilized”, but issues still arise ocassionally. Labor strikes have ended as unions negotiated their contracts.

Edwards conveyed his optimism: “When you look at the facts regarding age of fleets… affordability of vehicles… and how many great vehicles are being produced and put out there and how many new ones are coming in the funnel, if you will, into the market. This is all pent-up demand that’s going to be released at some point in the next 2 years. I think we all know that. And then hopefully, we have a 3-year run after” (J.P. Morgan Auto Conference, August 2023).

Operating leverage.

Edwards said that “both [European and North American] markets are operating significantly below the capacity that exists,” suggesting that increasing production volumes will have an outsized impact on profits (J.P. Morgan Auto Conference, August 2023).

Electric and hybrid vehicle opportunities due to increased complexity.

CPS provides the following number of parts for each vehicle type:

Internal Combustion Engines (ICE): 8 parts.

Hybrid: 28 parts.

Electric Vehicles (EV): 20 parts.

Edwards estimates the Content Per Vehicle or “CPV” (the total dollar value of parts supplied) is 20% higher for EVs as compared to ICE vehicles, and even higher for hybrids.

Innovative new product lines.

Examples of new product innovations include:

eCoFlow: Integrated fluid system that reduces complexity, increases efficiency and CPV. This product increases margins for CPS while also lowering total costs for the OEM customer.

Thermoplastic Body Door Seal: Sustainable dynamic seal that reduces weight, with color options, that requires less energy to produce as compared to traditional EPDM (synthetic rubber) material.

Fortrex: Lightweight thermosetting elastomer that also has applications to footwear, transportation, building and construction, and tires.

Edwards said that fortrex is generating $100 million in non-automotive sales and has the ability to grow to $200 million with 20% EBITDA or $40 million with additional investment.

Live Line Technologies: Proprietary AI-based Advanced Process Controls (APC) system which was developed to improve efficiency and reduce scrap. As a result, scrap rates have been cut in half, and unplanned downtime of machines due to line issues has also been reduced. The technology is now being marketed to external customers in a wide range of companies/industries, with one commercial order from a large fiber optic manufacturer.

By implementing digital analytics and AI, Edwards said they were able to spend less on engineering ($79 million this year as compared to $130 million in prior years) while launching more products.

During the third quarter, CPS was “awarded contracts for $91 million in annualized future sales on programs that include our most recent technology innovations” (Edwards, Q3 2023 earnings call). This represents about 3% of total revenue (~$2.5 billion in 2022).

Operational improvements resulting in a lean cost structure.

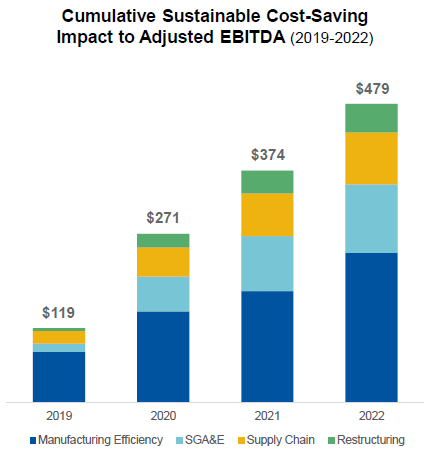

CPS has taken ~$480 million cumulative out of their cost structure (~$120 million annualized) over 2019-2022. Edwards said, “we’re leaner and more competitive than we’ve ever been” (J.P. Morgan Auto Conference, August 2023).

Edwards said they’re utilizing advanced analytics and AI to increase speed to market, eliminate physical samples, and eliminate testing. Additionally, the Company spent $79 million on engineering as compared to $130 previously, with more products launched.

To protect against volatile commodity prices in recent years, CPS negotiated index-based commercial agreements to partially recover cost increases and expected to complete negotiating all existing pricing contracts through EOY 2023.

Aligned Management Team and ROIC focus.

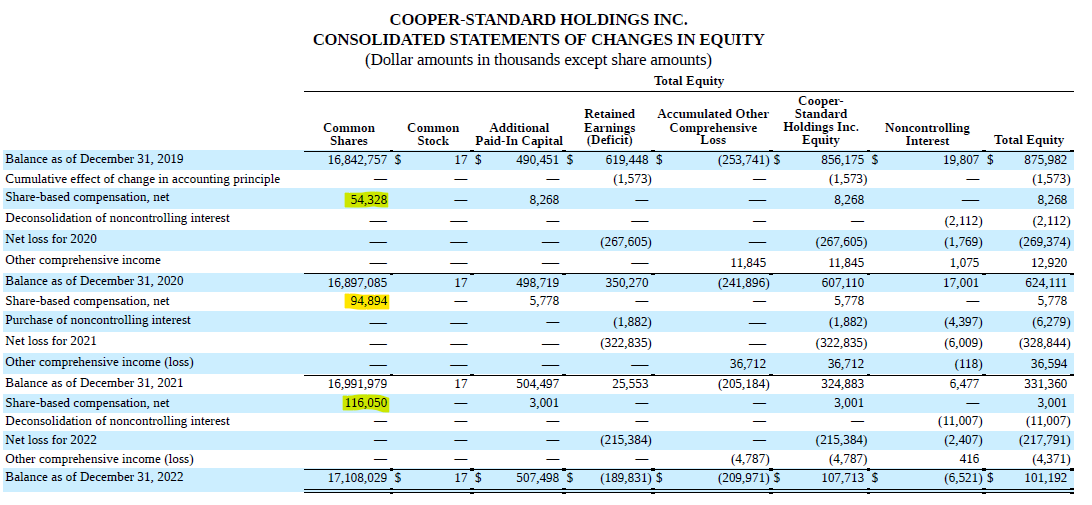

Share-based compensation is tied to ROIC, demonstrating an alignment of interests with shareholders.

“Financial Performance RSU [restricted stock units] payout is based on the Company’s capital efficiency during two, one-year performance periods (2022 and 2023). TSR [“total shareholder return”] Performance RSU payout is based on the Company’s RTSR [“relative total shareholder return”] performance versus a pre-established comparator group over the three-year performance period (2022-2024). We believe Performance RSUs align the interests of our NEOs [“named executive officers”] with those of our stockholders and further emphasize the importance of our long-term performance” (2022 Proxy Statement DEF 14-A).

The company requires minimum stock ownership levels as compared to executives’ salaries:

CEO: 6X multiple of base salary.

CFO: 3X multiple of base salary.

All other executives: 2X multiple of base salary.

Edwards owned 327,615 shares as of March 2023, as reported in his most recent S-4 filing. This represents ~2% of the company or ~$5 million.

Edwards said they are “laser-focused” on ROIC, which they expect to reach double-digits in the coming years. Additionally, Edwards said they will consider “divesting non-core businesses that don’t meet our strategic minimum rates for margins, ROI or future growth”. The company divested their European technical rubber business during Q3 2023.

Risks:

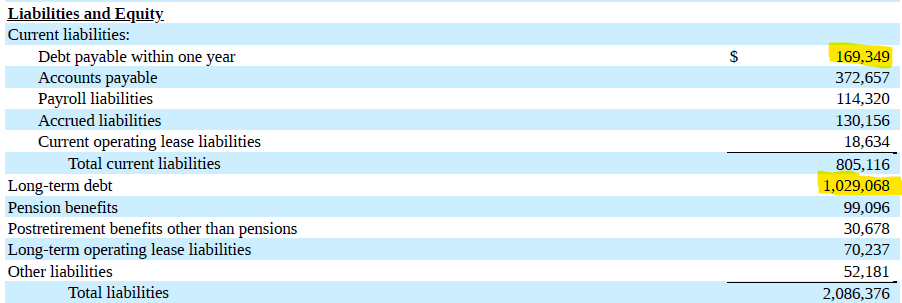

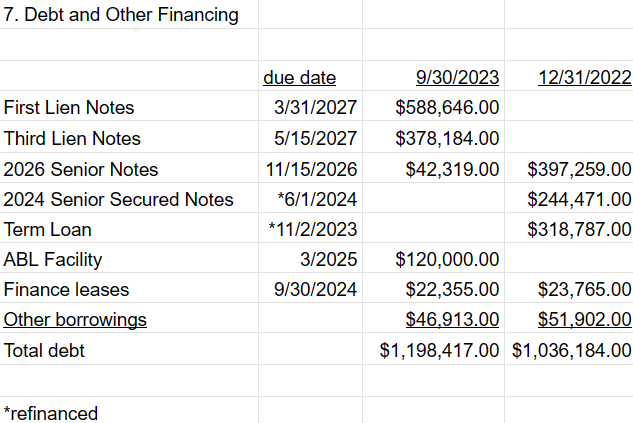

Debt: The company holds ~$1.2 billion of debt which management will prioritize paying down over the next few years as production ramps up. Below shows the liabilities as of 9/30/2023:

The schedule below breaks down the debt as of 9/30/2023:

Edwards expressed confidence that increased industry-wide production will enable the company to pay down the debt meaningfully by March of 2025, when the first loan comes due (the ABL facility). The company has held significant debt for many years; therefore, debt could be viewed as part of the capital structure rather than an indication of endless troubles.

Competition: Edwards said there is meaningful and “formidable” competition, and he expects consolidation over time.

Cyclicality: Recessions could have a significant impact on the business.

Share Repurchases:

The company authorized a share repurchase plan of $150 million beginning November 2018 and has $98.7 million remaining as of 9/30/2023. All repurchases after 2018 relate to “employee tax withholding requirements due upon the vesting of restricted stock awards”. Share count has increased annually by approximately 0.5-1.0% during 2019 through 2022 due to share-based compensation:

Volatility:

The stock is highly volatile due to its leverage and cyclicality. This adds downside risk, but also creates opportunity to trade shares at both despondent and exuberant extremes in sentiment and cyclicality. CPS peaked on 8/3/2018 at $146.78 (a ~21x multiple on its $7 EPS in 2017), then began its dramatic descent due to trade war concerns, then continued dropping throughout the post-covid supply chain challenges. It reached its low at $3.53 (a staggering 97.6% decline!) on 6/16/2022 due to bankruptcy fears from which it quickly rebounded as they refinanced debt.

Conclusion:

Cooper Standard offers a compelling bet on the automotive industry after several years of disruptions including post-covid supply chain challenges, a record aging fleet of U.S. vehicles, and labor union strikes. If auto production recovers as expected, we may see a return to 2017 profitability of $135 million or $7 EPS, which would make today’s $17 share price look like a bargain. There is room for further upside due to the improved lean cost structure, additional profits from new product offerings, and higher margin products serving EV and hybrid vehicles. Additionally, management is openly focused on achieving double-digit ROIC as demonstrated by their compensation structure. The potentially massive upside comes with risks relating to cyclicality and leverage that should be managed with an appropriate position size in one’s portfolio.

Legal and Disclaimer:

THE INFORMATION CONTAINED ON THIS WEBSITE IS NOT AND SHOULD NOT BE CONSTRUED AS INVESTMENT ADVICE, AND DOES NOT PURPORT TO BE AND DOES NOT EXPRESS ANY OPINION AS TO THE PRICE AT WHICH THE SECURITIES OF ANY COMPANY MAY TRADE AT ANY TIME. THE INFORMATION AND OPINIONS PROVIDED HEREIN SHOULD NOT BE TAKEN AS SPECIFIC ADVICE ON THE MERITS OF ANY INVESTMENT DECISION. INVESTORS SHOULD MAKE THEIR OWN DECISIONS REGARDING THE PROSPECTS OF ANY COMPANY DISCUSSED HEREIN BASED ON SUCH INVESTORS’ OWN REVIEW OF PUBLICLY AVAILABLE INFORMATION AND SHOULD NOT RELY ON THE INFORMATION CONTAINED HEREIN.

The information contained on this website has been prepared based on publicly available information and proprietary research. The author does not guarantee the accuracy or completeness of the information provided in this document. All statements and expressions herein are the sole opinion of the author and are subject to change without notice.

Any projections, market outlooks or estimates herein are forward looking statements and are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur. Other events that were not taken into account may occur and may significantly affect the returns or performance of the securities discussed herein. Except where otherwise indicated, the information provided herein is based on matters as they exist as of the date of preparation and not as of any future date, and the author undertakes no obligation to correct, update or revise the information in this document or to otherwise provide any additional materials.

The author, the author’s affiliates, and clients of the author’s affiliates may currently have long or short positions in the securities of certain of the companies mentioned herein, or may have such a position in the future (and therefore may profit from fluctuations in the trading price of the securities). to the extent such persons do have such positions, there is no guarantee that such persons will maintain such positions.

Neither the author nor any of its affiliates accepts any liability whatsoever for any direct or consequential loss howoever arising, directly or indirectly, from any use of the information contained herein. In addition, nothing presented herein shall constitute an offer to sell or the solicitation of any offer to buy any security.